Skip to content

Skip to content Streamline Your CSRD Compliance with Lythouse

Understanding CSRD Compliance

Effective from 2024, the Corporate Sustainability Reporting Directive (CSRD) mandates EU companies to disclose detailed environmental, social, and governance (ESG) information with the same scrutiny as financial data.

Check Your CSRD Compliance and Timeline

Public-interest enterprises

subject to NFRD

- More than 500 employees.

- Turnover of €50M+.

- Balance sheet of over €25M.

Report on financial year 2024 data to be published during calendar year 2025.

EU Large companies

- More than 250 employees.

- Turnover of €50M+.

- Balance sheet of over €25M.

Report on financial year 2025 data to be published during calendar year 2026.

Listed EU SMEs

- More than 50 employees.

- Turnover of €900K+.

- Balance sheet of over €450K.

Report on financial year 2026 data to be published during calendar year 2027.

Large companies

(Non-EU )

- EU generated turnover of €150M+.

- A branch in the EU generating more than €40M.

Report on financial year 2028 data to be published during calendar year 2029.

Note: SMEs may opt-out of CSRD application for two years, exempting them from publishing CSRD disclosures until 2029.

ESRS Data Requirements for CSRD Compliance

ESRS 1

ESRS 2

ESRS Data Requirements for CSRD Compliance

ESRS 1

|

Double materiality assessment |

Sustainability due diligence |

|---|---|

|

Supply and value chain |

Timeline |

ESRS 2

|

Governance 1-5 Disclosure |

Strategy: SBM 1-3 |

|---|---|

|

Impacts, risks and opportunities - IRO 1-2 |

Metrics and targets |

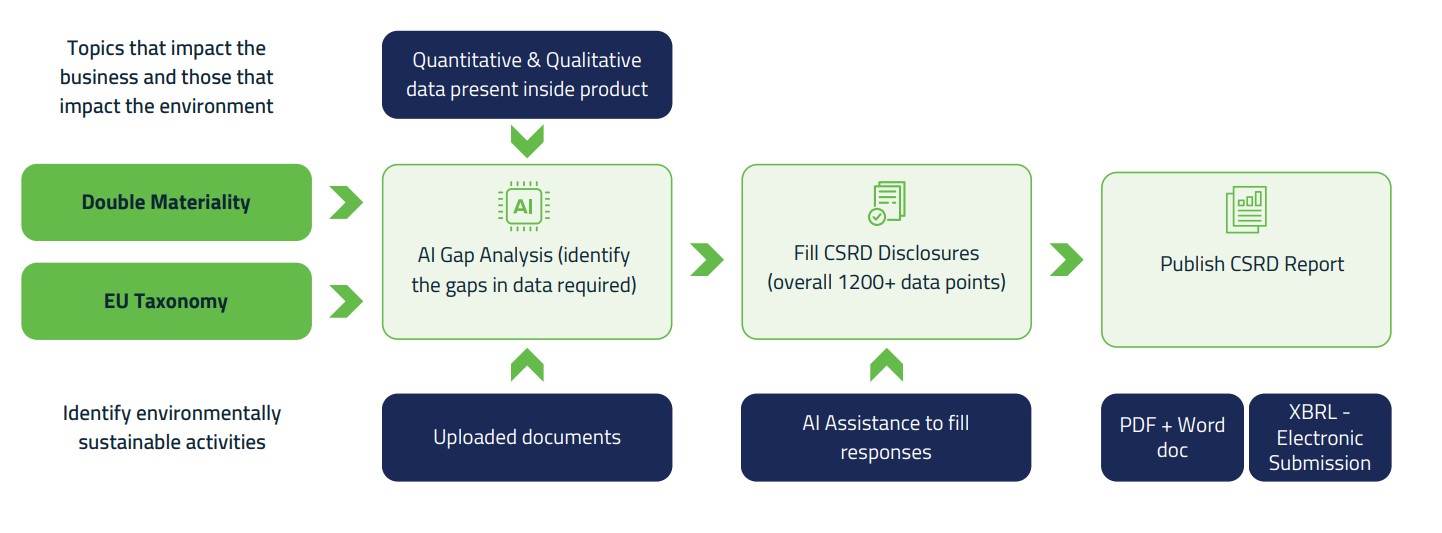

Effortlessly Navigate CSRD Compliance with Lythouse

Double Materiality

EU Taxonomy

Quantitative & Qualitative data present inside product

AI Gap Analysis (identify the gaps in data required)

Double Materiality

Fill CSRD Disclosures (overall 1200+ data points)

AI Assistance to fill responses

Publish CSRD

Report

PDF + Word doc

XBRL - Electronic Submission

Make Informed Decisions with Double Materiality

Lythouse simplifies this by identifying key sustainable topics, auto-selecting relevant issues, and integrating these results into your CSRD report. This approach ensures comprehensive, compliant disclosures, streamlining ESG reporting under CSRD.

Ensure Sustainable Investments with EU Taxonomy

Intelligent ESG Data Management and Gap Analysis

Seamlessly connect your existing systems (CRM, ERP, HR) to gather data on spending, consumption, travel, and more. Utilize Merlin AI to perform detailed gap analysis on the collected data, scanning for missing information and auto-populating it to ensure precise, comprehensive, and CSRD-compliant reporting.

Advanced Approval Workflows and Audit Trails

Data Validation

Implement configurable approval workflows, with POCs reviewing and approving data before audits.

Audit Trails

Ensure complete traceability by recording every action and modification, supporting all types of audits.

Export Capabilities

Seamlessly export reports to DOC and XBRL formats for easy sharing and regulatory submission.