Skip to content

Skip to content

This blog delves into CSRD double materiality, a foundational concept in the Corporate Sustainability Reporting Directive (CSRD). It explores how this approach goes beyond traditional reporting to provide a holistic view of an organization’s impact.

Double materiality is a foundational concept in the Corporate Sustainability Reporting Directive (CSRD) that addresses the dual perspectives of how sustainability issues impact an organization’s financial performance and how the organization’s activities impact the environment and society. This approach represents a significant advancement in corporate sustainability reporting, acknowledging that the risks and opportunities associated with environmental, social, and governance (ESG) issues are intertwined with an organization’s financial health and its broader impacts on society.

A recent study by McKinsey & Company found that companies with strong ESG performance outperform their peers financially in the long term. This underscores the financial relevance of environmental and social considerations.

Understanding CSRD Double Materiality

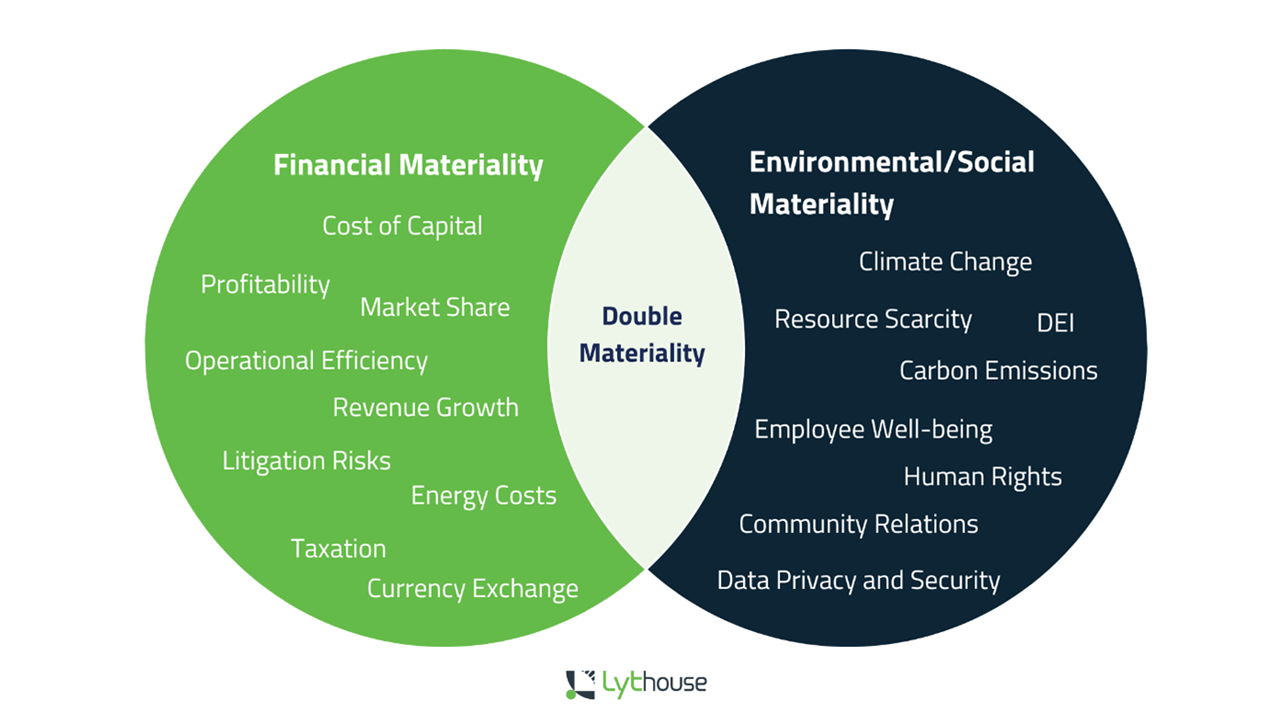

Definition: Double materiality combines two distinct types of materiality assessments: financial materiality and environmental/social materiality. Financial materiality focuses on the implications of ESG issues on an organization’s financial condition and operating performance, while environmental/social materiality considers the organization’s impact on people and the planet.

CSRD Double Materiality Assessment: This involves a thorough evaluation to identify and prioritize ESG issues that are materially significant from both financial and environmental/social perspectives. Organizations are required to report on these issues, detailing their impacts, the risks and opportunities they pose, and how they are being managed.

Why Double Materiality is Essential for CSRD

A survey by PwC revealed that 83% of investors consider ESG factors when making investment decisions. Double materiality reporting provides investors with the information they need to assess a company’s sustainability risks and opportunities.

Double materiality is crucial for CSRD compliance because it ensures that reporting captures the full spectrum of an organization’s sustainability performance. Unlike traditional financial reporting, which primarily focuses on financial impacts, double materiality:

- Enhances transparency and accountability by revealing how organizations contribute to or mitigate sustainability challenges.

- Provides stakeholders, including investors, customers, and regulators, with a comprehensive view of an organization’s sustainability efforts and financial resilience in the face of ESG risks.

The Diverse ESG Reporting Landscape: Standards, Frameworks, Rankers & Raters

| Category | Description | Key Players | Purpose |

| Reporting Standards | Detailed guidelines outlining specific metrics and disclosures companies must report on ESG performance. | * Global Reporting Initiative (GRI) * Sustainability Accounting Standards Board (SASB) * International Financial Reporting Standards (IFRS) Sustainability Reporting Standards | * Ensure consistency and comparability of ESG data across companies. * Enhance transparency and accountability in sustainability reporting. |

| Framework Developers | Voluntary sets of principles, recommendations, and guidance companies can use to structure their ESG disclosures. | * Task Force on Climate-Related Financial Disclosures (TCFD) * Climate Disclosure Standards Board (CDSB) * IIRC Integrated Reporting Framework | * Offer flexibility for companies to adapt to their specific industries and contexts. * Provide a starting point for companies developing ESG reporting practices. |

| Rankers | Assess and compare companies’ ESG performance based on publicly available information and may not involve direct engagement with companies. | * MSCI ESG Ratings * Sustainalytics * FTSE Russell ESG Ratings | * Provide investors with a relative comparison of companies’ ESG performance. * Can inform investment decisions and promote ESG integration into portfolios. |

| Raters | Conduct in-depth assessments of companies’ ESG practices, often through questionnaires, interviews, and engagement with company management. | * Moody’s ESG Solutions * S&P Global Corporate Sustainability Assessment * CDP (formerly Carbon Disclosure Project) | * Provide a more comprehensive and nuanced view of a company’s ESG performance. * Can be used by investors, lenders, and other stakeholders to make informed decisions. |

| Regulators | Establish rules and guidelines for ESG disclosure. | * Securities and Exchange Commission (SEC) (US) * European Commission (EU) | * Promote transparency and investor protection through mandated ESG disclosures. * Set minimum standards for ESG reporting within a jurisdiction. |

Comparing CSRD with SEC ESG Reporting

Unlike the European Union’s CSRD, which mandates double materiality assessment, the U.S. Securities and Exchange Commission’s (SEC) approach to ESG reporting primarily focuses on material risks to investors, closely aligning with the concept of financial materiality. This difference underscores the EU’s broader ambition to integrate sustainability into corporate governance and accountability, beyond the interests of financial stakeholders alone.

Identifying Double Materiality Topics

Identifying double materiality topics requires organizations to:

- Conduct stakeholder engagement to understand which ESG issues are most important to their stakeholders and the environment/society at large.

- Assess the significance of these issues in terms of their potential financial impact on the organization.

- Evaluate the organization’s impact on environmental and social matters.

Simplifying Double Materiality Assessment with Software Tools

Software tools, like Lythouse, play a critical role in simplifying the complex task of identifying and assessing double materiality topics. These tools can:

- Provide frameworks and guidelines aligned with EU CSRD requirements, ensuring comprehensive and compliant reporting.

- Automate data collection and analysis across the 1200 data points specified in CSRD, including the identification of DMA (Double Materiality Assessment) and EU taxonomy-related information.

- Facilitate stakeholder engagement through surveys and collaboration features, allowing for a broad range of inputs to inform the materiality assessment process.

- Generate insights and visualizations, such as materiality matrices, that clearly delineate the financial and environmental/social dimensions of materiality, assisting organizations in prioritizing their sustainability initiatives.

Download e-Book on Gen-AI for ESG Data Management

Latest Trends and Insights in CSRD Double Materiality

1. Understanding the Value Chain in Double Materiality

In the realm of CSRD, appreciating the full scope of your value chain—from raw material sourcing to end-product disposal—is critical. This analysis aids in pinpointing where your company can make significant sustainability impacts or face risks and opportunities. For instance, consider the indirect emissions (Scope 3) which often constitute the bulk of a company’s carbon footprint. By mapping out these interactions within your value chain, you can identify key areas for sustainability initiatives and regulatory compliance, providing a comprehensive picture that goes beyond direct operational impacts.

2. Effective Stakeholder Engagement Strategies

Stakeholder engagement is pivotal in shaping a robust double materiality framework. Utilize diverse engagement platforms such as digital surveys, interactive workshops, and targeted focus groups to gather rich, qualitative data from your stakeholders. This approach ensures that the sustainability issues prioritized are those that truly resonate with both internal and external parties. It’s also essential for maintaining transparency and building trust, as stakeholders are more likely to support initiatives they had a hand in shaping.

3. Identifying and Scoring Impacts, Risks, and Opportunities (IROs)

Begin with a detailed identification process for potential impacts, risks, and opportunities related to environmental, social, and governance (ESG) factors. This should involve gathering data from various sources, including internal operations, stakeholder feedback, and industry benchmarks. Develop a scoring system that evaluates the severity and likelihood of these IROs, which will help prioritize them based on their potential financial and social impact. This structured assessment allows companies to allocate resources more effectively and address the most pressing sustainability challenges.

4. Aligning with European Sustainability Reporting Standards (ESRS)

To ensure CSRD compliance, align your double materiality findings with ESRS metrics. This integration involves detailing how each relevant ESRS metric is addressed within your report. Utilizing software solutions for tracking and reporting these metrics can greatly enhance the efficiency, accuracy, and security of your data. It also simplifies the compliance process, ensuring that all necessary disclosures are accurate and complete, thereby upholding the integrity of your sustainability reporting.

5. Continuous Monitoring and Dynamic Updates

Sustainability is a dynamic field, with evolving stakeholder expectations and regulatory requirements. Establish a systematic process for regularly reviewing and updating your materiality assessments. This could include annual reviews or more frequent checks in response to significant operational changes or external factors. Such ongoing vigilance ensures that your sustainability reporting remains relevant and reflective of current conditions, thereby maintaining its value and utility for decision-making.

6. From Compliance to Competitive Advantage

While compliance with CSRD is mandatory, there is significant strategic value in leveraging these requirements for competitive advantage. Transparent reporting and diligent sustainability practices can enhance corporate reputation, attract investment, and foster loyalty among customers and employees alike. By demonstrating leadership in sustainability, companies can differentiate themselves in the marketplace, turning regulatory compliance into an opportunity for brand enhancement and business growth.

Conclusion

Double materiality represents a paradigm shift in corporate sustainability reporting, emphasizing the interconnectedness of financial performance and sustainability impacts. As organizations navigate the complexities of CSRD compliance, tools like Lythouse offer essential support, streamlining the assessment process and enabling a more informed, strategic approach to sustainability.

The requirement for a double materiality assessment underlines the EU’s commitment to fostering a more sustainable, transparent, and resilient corporate sector, setting a benchmark for global sustainability reporting standards. Book a demo today!

FAQs

1: What is the primary objective of the CSRD?

Answer: The main goal of the Corporate Sustainability Reporting Directive (CSRD) is to enhance transparency in sustainability reporting across the EU, aiming to support the transition to a sustainable economy. This aligns with the European Green Deal and the UN Sustainable Development Goals by ensuring that stakeholders have reliable and comparable information to assess sustainability risks and impacts.

2: Which entities are required to comply with the CSRD?

Answer: The CSRD expands the scope of the previous Non-Financial Reporting Directive (NFRD) and applies to around 50,000 entities, including those with securities listed on EU markets and large companies meeting specific financial thresholds. This includes entities with net turnover exceeding €40 million, total assets over €20 million, or more than 250 employees.

3: When do entities need to start reporting under CSRD?

Answer: Reporting under CSRD begins for financial years starting on or after January 1, 2024. The first entities to report will be those already covered under the NFRD, with other large entities following in subsequent years. Reporting requirements will gradually extend to include SMEs and subsidiaries by fiscal year 2028.

4: What are the key differences between NFRD and CSRD?

Answer: The CSRD introduces more rigorous reporting requirements with the implementation of European Sustainability Reporting Standards (ESRS), which demand that sustainability information is integrated into the annual management reports. This differs from the NFRD by broadening the scope and enhancing the detail and comparability of the reports.

5: How does the CSRD integrate with other EU regulations like the SFDR and EU Taxonomy?

Answer: The CSRD is part of the EU’s broader Sustainable Finance Framework, which includes the SFDR and EU Taxonomy. It complements these regulations by providing detailed reporting standards (ESRS) that align with and support disclosures required under both the SFDR and the Taxonomy, facilitating a comprehensive view of sustainability impacts and performance.

6: What are the implications of CSRD for non-EU entities?

Answer: Non-EU entities with significant operations or listings in the EU are also subject to CSRD if they meet certain criteria. This includes having a large subsidiary or a significant economic presence within the EU. These entities will need to comply with CSRD mandates regarding sustainability disclosures, even if their primary operations are based outside of the EU.

Sonal is leading product and content marketing initiatives at Zycus. She is a problem solver. She has a proven track record of defining positioning and messaging for various product modules, creating go-to-market strategies for new features and product launches, and fostering collaboration between Product Management, Sales, and Customer Success teams.