Skip to content

Skip to content

Introduction: A New Dawn in Corporate Transparency

Imagine a world where every product you use, every service you enjoy, comes with a story—not just of its origin but of its journey. A story that accounts for every ripple it creates in the world, from the spark of its creation to its final farewell. This is the world the Corporate Sustainability Reporting Directive (CSRD) envisions, with its comprehensive embrace of Scope 3 emissions, shining a light on the often-overlooked corners of a company’s environmental impact.

The Heart of CSRD: Why Scope 3 Takes Center Stage

In the intricate dance of sustainability reporting, CSRD Scope 3 emissions take the lead, guiding companies beyond the familiar terrain of direct operations (Scope 1) and purchased energy (Scope 2), into the vast expanse of the value chain. It’s here, in the aggregate of all other indirect emissions, that the true scale of a company’s environmental footprint is revealed. Whether it’s the emissions from the materials sourced or the end-life of products, Scope 3 captures the entirety of a company’s impact on the planet.

Why Scope 3 Is the Linchpin of Environmental Accountability

- A Kaleidoscope of Impact: Scope 3 emissions account for, on average, up to 75% of a company’s carbon footprint, dwarfing the direct emissions (Scope 1) and the indirect emissions from purchased energy (Scope 2). This vast expanse includes all indirect emissions, from the extraction of raw materials to product end-of-life, offering a comprehensive view of a company’s environmental impact.

- The Challenge of Transparency: Mapping out Scope 3 emissions is akin to charting a course through uncharted waters. It requires not only an understanding of one’s own operations but also a deep dive into the practices of suppliers, partners, and distributors. The complexity of this endeavor is matched only by its potential to drive substantial change, encouraging companies to foster sustainability throughout their value chain.

- A Catalyst for Innovation: Addressing CSRD Scope 3 emissions spurs companies to reimagine their processes, products, and partnerships. It opens the door to innovative solutions like circular economy models, sustainable sourcing practices, and efficiency improvements. By tackling Scope 3, companies can turn sustainability challenges into competitive advantages, paving the way for new business models and opportunities.

However, as with any worthwhile endeavor, the path to achieving significant reductions in this area isn’t without its hurdles. There’s an age-old adage that rings true here: the greatest things are often the hardest to measure. Quantifying the environmental impact of a complex network of suppliers, partners, and far-flung operations presents a unique challenge. Let’s delve deeper into the specific obstacles companies face when it comes to measuring CSRD Scope 3 emissions.

1. The Complexity of the Value Chain

In the vast ecosystem of corporate operations, the value chain resembles a sprawling metropolis, buzzing with activity at every corner. From raw material sourcing to end-of-life disposal, each step is a cog in the vast wheel of Scope 3 emissions. Under the CSRD, companies are tasked with mapping this intricate network—a Herculean task that requires not just internal diligence but also transparency and cooperation from every partner in the chain. This exhaustive mapping process is akin to charting the constellations in the night sky, where each star represents a supplier, partner, or indirect operation contributing to the company’s Scope 3 emissions.

2. Data Availability and Quality

Embarking on the CSRD Scope 3 journey often feels like setting sail in uncharted waters, where the compass of data points you in multiple directions. The challenge here is twofold: not only must companies collect vast amounts of data from myriad sources, but they must also ensure its accuracy and reliability. In the context of CSRD, the stakes are even higher, as reported data must withstand the scrutiny of stakeholders and comply with stringent reporting standards. The quest for high-quality data is akin to mining for gold—tedious, time-consuming, but ultimately rewarding in the pursuit of sustainability.

3. Standardization of Reporting

Within the diverse tapestry of industries, each thread follows its pattern, making standardization a formidable challenge. The CSRD seeks to weave these disparate threads into a cohesive narrative through uniform reporting standards. However, for companies

navigating the Scope 3 landscape, this requires not just internal adjustments but also alignment with external partners who may operate under different standards. This endeavor is akin to orchestrating a symphony where each musician plays a different tune, demanding a conductor’s precision to harmonize the performance.

4. Technological and Methodological Gaps

As companies traverse the CSRD Scope 3 terrain, they encounter the dual hurdles of technological and methodological gaps. The tools and techniques required to measure, track, and report indirect emissions are still evolving, presenting a significant barrier to comprehensive Scope 3 accounting. Under the CSRD, leveraging cutting-edge technology and adopting robust methodologies is paramount. Yet, for many, this represents a leap into the unknown, akin to building a bridge while crossing it, where each step forward is a test of innovation and resolve.

5. Engagement and Influence Across the Value Chain

Imagine trying to direct an orchestra where some musicians are miles away, unaware of your baton’s movements. This metaphor encapsulates the challenge of engaging with and influencing stakeholders across the value chain. The CSRD mandates a level of transparency and cooperation that many companies find daunting, requiring not just communication but also persuasion and partnership. Achieving CSRD Scope 3 emission reductions often hinges on this collaborative effort, turning distant partners into co-authors of the sustainability story.

A Categorical Breakdown of Scope 3 Challenges

The Greenhouse Gas Protocol (GHG Protocol) categorizes Scope 3 emissions into 15 categories further divided into upstream and downstream activities. To shed light on the specific challenges within each category, let’s delve deeper:

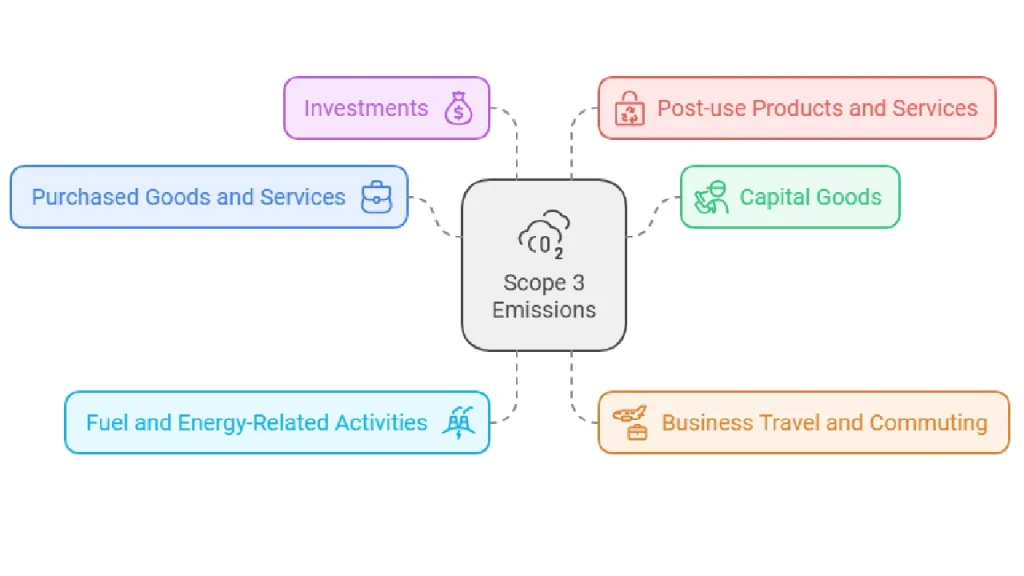

Category 1: Purchased Goods and Services (PGS)

Imagine a clothing retailer. While their Scope 1 emissions might include energy consumption in their stores, their Scope 3 footprint would be heavily influenced by the production processes of their suppliers – the cotton farming, fabric manufacturing, and garment assembly.

· Challenge: Obtaining reliable emissions data from suppliers, particularly those in geographically dispersed locations with varying environmental reporting practices.

A major furniture manufacturer struggled to accurately measure the carbon footprint of its wood supplies due to a lack of transparency from upstream forestry operations in Southeast Asia.

Category 2: Capital Goods

A car manufacturer’s Scope 3 footprint would be significantly impacted by the embodied emissions associated with the steel, aluminum, and other materials used in vehicle production.

· Challenge: Accounting for the complex life cycle stages of capital goods, including raw material extraction, processing, and transportation.

Category 3: Fuel and Energy-Related Activities Not Included in Scope 1 or 2 (FRAC)

Think of a logistics company. Their Scope 1 emissions would encompass fuel consumption in their delivery vehicles, but their Scope 3 footprint would extend to the emissions associated with fuel production and transportation (upstream FRAC).

· Challenge: A lack of standardized methodologies for calculating upstream FRAC emissions, leading to potential inconsistencies and inaccuracies in reporting.

Category 4: Business Travel and Commuting

· Challenge: Gathering comprehensive data on employee travel patterns, including personal vehicle usage, public transportation, and air travel.

Category 5: Investments

A financial institution’s Scope 3 footprint could be influenced by the emissions associated with the companies they invest in.

· Challenge: Limited influence over the environmental practices of investee companies, making data collection a significant hurdle.

Category 6: Post-use Products and Services

The end-of-life management of a product significantly impacts its overall environmental footprint. Consider a mobile phone manufacturer – their CSRD Scope 3 footprint would be influenced by the energy consumption and potential environmental hazards associated with e-waste disposal practices.

· Challenge: The lack of control over how consumers dispose of products and the limited availability of data on post-use emissions.

While Categories 1-6 represent the primary classifications within Scope 3, a deeper dive reveals even more granular subcategories like leased assets, franchises, processing losses, and waste generated in the use phase. Each subcategory presents its own unique challenges, from data availability in waste management (Category 3) to the complex life cycle assessment of leased assets (Category 1).

Taming the Beast: Effective Scope 3 Measurement

The inherent challenges of Scope 3 measurement lie in its very nature. Unlike Scope 1 and 2 emissions, which occur within a company’s direct control, Scope 3 encompasses a vast web of external actors and activities. Gathering accurate data from a geographically dispersed network of suppliers, piecing together fragmented information from various sources, and accounting for the intricate life cycle stages of products all contribute to the complexity of this exercise.

Traditionally, companies have relied on manual processes and spreadsheets to tackle Scope 3 measurement. However, this approach often falls short due to limitations in several key areas:

- Limited Visibility and Supplier Inconsistency: Manual communication with suppliers can be time-consuming and ineffective. Inconsistent reporting practices across diverse suppliers can lead to inaccurate or incomplete data.

- Data Silos and Inconsistencies: Scattered data across multiple spreadsheets and sources creates a challenge in data consolidation and triangulation. Manual data entry increases the risk of errors and inconsistencies.

- Lack of Granularity: Relying solely on generic emission factors or industry averages overlooks the nuances of specific products and processes. Limited access to item-level data and supplier-specific life cycle assessments (LCAs) hinders the accuracy of calculations.

The Way Ahead

Fortunately, a more effective approach exists. Software platforms specifically designed for Scope 3 measurement offer a powerful solution by addressing these challenges head-on. These platforms go beyond simply automating data collection. They facilitate a coherent combination of data sources and functionalities that work together to deliver a more accurate picture of your company’s environmental footprint.

| Aspect | Manual Approach Challenges | Software Platform Advantages |

| Supplier Coordination | Manual communication, limited visibility into supplier practices | Streamlined communication tools, supplier engagement modules, data collection templates |

| Triangulation of Spend Data | Multiple spreadsheets, data inconsistencies | Centralized data repository, automated data integration with ERP systems |

| Item-Level Data & Supplier Information | Limited access to granular product data, reliance on generic emission factors | Product databases with life cycle assessments (LCAs), supplier information portals |

A recent study by McKinsey & Company found that companies using digital solutions for Scope 3 measurement can achieve a 20-30% improvement in data accuracy compared to manual methods. This enhanced accuracy translates into a more robust understanding of your company’s true environmental footprint, enabling you to set realistic reduction targets and demonstrate progress towards sustainability goals.

For instance, a leading consumer goods company struggled to accurately measure the Scope 3 emissions associated with their vast network of suppliers. Manually collecting data from hundreds of suppliers across the globe proved time-consuming and prone to errors. Implementing a sustainability software platform facilitated streamlined communication, standardized data collection templates, and the integration of supplier-specific LCA data. This resulted in a 15% reduction in estimated Scope 3 emissions compared to their previous manual calculations, providing a more accurate picture of their environmental impact.

Watch our comprehensive Webinar – The Power of Partnerships: Transforming the Governance of Scope 3 Data Collection

Latest Trends in CSRD Scope 3 Emissions Reporting

1. Double Materiality and its Implications

- Definition and Importance: Double materiality is a key concept under CSRD, requiring companies to assess and report both the financial impacts of sustainability issues on the company and the company’s impacts on society and the environment. This dual focus ensures comprehensive sustainability reporting.

- Implementation Steps: Companies need to conduct double materiality assessments by engaging stakeholders, identifying material ESG topics, and integrating findings into their strategy and reporting processes.

- Benefits and Challenges: This approach enhances transparency and accountability but can be challenging due to the extensive data collection and stakeholder engagement required.

2. Engaging the Value Chain for Scope 3 Emissions

- Upstream and Downstream Emissions: Scope 3 emissions include all indirect emissions from a company’s value chain, both upstream (suppliers, raw materials) and downstream (product use, disposal).

- Collaboration Strategies: Successful management of Scope 3 emissions requires close collaboration with suppliers and customers to collect accurate data and implement reduction strategies. This includes establishing clear communication channels and setting joint sustainability goals.

- Technological Solutions: Leveraging digital tools and platforms, such as supplier management systems and blockchain technology, can enhance data collection and tracking across the value chain.

3. Leveraging Technology for Accurate Scope 3 Reporting

- Data Management Platforms: Implementing robust data management systems that centralize and standardize emissions data is crucial for accurate reporting. These platforms can facilitate real-time data collection and analysis.

- Innovative Tools: Technologies like IoT, AI, and blockchain can provide real-time monitoring and improve the transparency of emissions data throughout the supply chain.

- Case Studies: Highlight successful implementations of technology in Scope 3 reporting, showcasing companies that have effectively used these tools to improve their sustainability reporting and performance.

4. Regulatory Requirements and Compliance under CSRD

- Overview of CSRD Requirements: The CSRD mandates detailed sustainability reporting, including Scope 3 emissions, for companies operating in the EU. It emphasizes the importance of granular emissions disclosure and the establishment of emission reduction targets.

- Compliance Timeline: Large companies must start reporting in 2024, with different deadlines for other types of entities. Compliance involves integrating CSRD standards into existing reporting frameworks and ensuring data accuracy and completeness.

- Third-Party Assurance: The CSRD requires that reported sustainability data be verified by an independent third-party auditor to ensure accuracy and reliability. This adds an additional layer of accountability and trust in the reported data.

5. Developing a Comprehensive Scope 3 Emissions Reduction Strategy

- Setting Targets: Establishing clear, measurable targets for reducing Scope 3 emissions is essential. These targets should be aligned with broader corporate sustainability goals and regulatory requirements.

- Action Plans: Companies need to develop detailed action plans that outline specific steps to achieve emission reduction targets. This includes investing in sustainable technologies, redesigning products for lower emissions, and improving operational efficiencies.

- Stakeholder Engagement: Engaging with stakeholders, including suppliers, customers, and investors, is crucial for the success of Scope 3 reduction strategies. This involves regular communication, collaboration, and transparency about progress and challenges.

6. Challenges and Opportunities in Scope 3 Reporting

- Data Quality and Availability: One of the main challenges in Scope 3 reporting is obtaining high-quality data from the entire value chain. Companies must work to overcome these challenges by establishing robust data collection processes and ensuring data accuracy.

- Regulatory Pressure and Market Demand: Increasing regulatory requirements and market demand for transparency and sustainability are driving companies to improve their Scope 3 reporting practices. This also presents opportunities for companies to differentiate themselves through superior sustainability performance.

- Innovative Solutions: Adopting innovative solutions and technologies can help companies navigate the complexities of Scope 3 reporting and leverage these challenges as opportunities for improvement and leadership in sustainability.

Case Studies

Case Study 1: IKEA’s Approach to Scope 3 Emissions

Overview: IKEA is well-known for its dedication to sustainability. The company places a strong emphasis on minimizing its environmental impact throughout its entire value chain, from product design to the disposal of products.

Scope 3 Initiatives:

- IKEA has implemented a comprehensive supplier engagement program to ensure that its extensive network of suppliers adheres to strict environmental standards. This includes regular sustainability audits and the provision of training and resources to help suppliers reduce their carbon emissions.

- The company has invested in renewable energy projects at its suppliers’ sites to decrease carbon emissions. For example, it has installed solar panels at many supplier locations.

- IKEA actively works towards circular economy principles, designing products for longevity and recyclability, and encouraging product take-back schemes to manage the end-of-life impact.

Impact: These initiatives have allowed IKEA to make significant progress in reducing its Scope 3 emissions. By involving every actor in its supply chain, IKEA not only reduces its environmental impact but also sets a benchmark in the industry for sustainability practices.

Case Study 2: Unilever’s Sustainable Living Plan

Overview: Unilever’s Sustainable Living Plan sets out a series of targeted strategies aimed at reducing their environmental footprint and increasing their positive social impact.

Scope 3 Initiatives:

- Unilever has focused on decarbonizing its logistics operations to tackle Scope 3 emissions related to transportation and distribution. This includes optimizing routes, using vehicles that are more fuel-efficient, and experimenting with alternative fuels like biofuels and electric vehicles.

- The company engages with its consumers to tackle emissions associated with the use of their products, which forms a significant part of their Scope 3 emissions. This includes campaigns and incentives to encourage consumers to select lower-carbon options and sustainable product use practices.

- Unilever works closely with its suppliers to reduce emissions by helping them adopt more sustainable practices and technologies.

Impact: These efforts have contributed to Unilever’s ability to significantly reduce its Scope 3 emissions, demonstrating leadership in corporate sustainability and providing a replicable model for other companies.

How Lythouse can assist with CSRD Scope 3 Reporting

Lythouse offers tools designed to streamline CSRD Scope 3 compliance and enhance sustainability reporting. The Carbon Analyzer precisely tracks and reports Scope 3 emissions across the supply chain, ensuring accuracy and transparency. The ESG Reporting Studio facilitates the integration of comprehensive data into reports that meet CSRD requirements. The Goal Navigator aids in setting and achieving emissions reduction targets, aligning with Scope 3 objectives. Finally, the Green Supplier Network enhances supplier engagement and data collection, critical for accurate Scope 3 reporting. Together, these tools empower companies to fulfill regulatory requirements and advance their sustainability goals.

By leveraging the power of software platforms, companies can navigate the complexities of Scope 3 measurement with greater confidence, paving the way for a more sustainable future. Book a demo today!

FAQ’s

1.What does CSRD Scope 3 mean?

CSRD Scope 3 refers to the part of the Corporate Sustainability Reporting Directive that deals with reporting indirect emissions not produced by the company itself but related to its value chain. This includes both upstream and downstream emissions, such as those from purchased goods, transportation services, and waste disposal.

2. What is CSRD?

The CSRD (Corporate Sustainability Reporting Directive) is an EU regulation that extends and strengthens the existing non-financial reporting requirements. It aims to provide greater transparency on the sustainability aspects of companies, ensuring that large firms publicly disclose information on their environmental, social, and governance (ESG) impacts, risks, and opportunities.

3. What are Scope 3 emissions?

Scope 3 emissions are a category of indirect emissions that result from activities not owned or directly controlled by the reporting company but that the company indirectly impacts in its value chain. This includes emissions associated with the production of purchased goods and services, business travel, employee commuting, waste disposal, use of sold products, and transportation and distribution.

4. What are Scope 3 emissions in the context of CSRD?

Scope 3 emissions refer to indirect emissions that occur in a company’s value chain, including both upstream and downstream emissions. These are emissions that the company does not directly control but are part of its entire supply chain, from the production of purchased goods and services to end-of-life treatment of sold products.

5. How does CSRD impact the reporting of Scope 3 emissions?

The Corporate Sustainability Reporting Directive (CSRD) enhances transparency by requiring companies to disclose detailed information about their Scope 3 emissions if they are material to the business. This is part of broader efforts to ensure companies acknowledge and manage their entire carbon footprint.

6. What challenges do companies face when reporting Scope 3 emissions under CSRD?

Reporting Scope 3 emissions can be complex due to the need to gather data from multiple sources, some of which the company does not directly control. The accuracy of this data and ensuring it is comprehensive are among the key challenges companies face.

7. How can companies prepare for CSRD compliance concerning Scope 3 emissions?

Companies can prepare by establishing robust systems for data collection and management, engaging with suppliers to ensure data accuracy, and implementing software solutions that facilitate the aggregation and reporting of emissions data. Adopting a phased approach to compliance, as outlined in the CSRD, helps companies adjust their processes gradually.

Amelia Rose is a leading expert in Environmental, Social, and Governance (ESG) issues. She brings a deep understanding of ESG, sustainability, climate change, sustainable development, and corporate social responsibility to her work. Rose has extensive experience in consulting with businesses and organizations on developing and implementing effective ESG strategies. She is a passionate advocate for a greener future and believes that businesses can be a powerful force for positive change.